If you are an NRI earning income from Indian properties, investments, or bank accounts — India’s tax law applies to you. This guide cuts through the complexity: what is taxable, what is exempt, how TDS works, and how FinCirc India helps you stay fully compliant without overpaying a single rupee.

Who Is an NRI for Income Tax Purposes?

Your tax liability in India depends entirely on your residential status under the Income Tax Act, 1961 — not your citizenship or passport. This status is determined fresh every financial year (April 1 to March 31).

You are classified as an NRI (Non-Resident Indian) for a given financial year if you have spent fewer than 182 days in India during that year. There is an additional test: if you stayed fewer than 60 days in the current year and fewer than 365 days in the preceding four years combined, you are also classified as an NRI.

Three Residential Status Categories You Must Know

Resident (ROR): Taxed on worldwide income — both Indian and foreign. Most returned NRIs eventually fall here.

RNOR (Resident but Not Ordinarily Resident): A transitional status for returning NRIs. Only Indian-source income is taxed. Available for two years after returning to India.

NRI (Non-Resident): Only income earned or received in India is taxable. Foreign income is completely outside India’s tax net.

Important 2025 Update: The Income Tax Bill 2025, which is expected to come into force on April 1, 2026, retains the existing NRI tax residency rules. NRIs earning ₹15 lakh or more in India who do not pay taxes abroad will continue to be classified as RNOR — ensuring only Indian-source income is taxed.

What Income Is Taxable for NRIs in India?

As an NRI, India taxes only the income that arises in India or is received in India. Your salary earned in the USA, rent from a flat in the UK, or dividends from foreign stocks — none of these attract Indian tax while you remain an NRI.

Income That Is Taxable for NRIs

- Salary: If you perform services in India, that salary is taxable even if paid into a foreign account.

- Rental income: Rent from any property located in India is fully taxable.

- Capital gains: Gains from selling Indian shares, mutual funds, or property are taxable in India regardless of where you live.

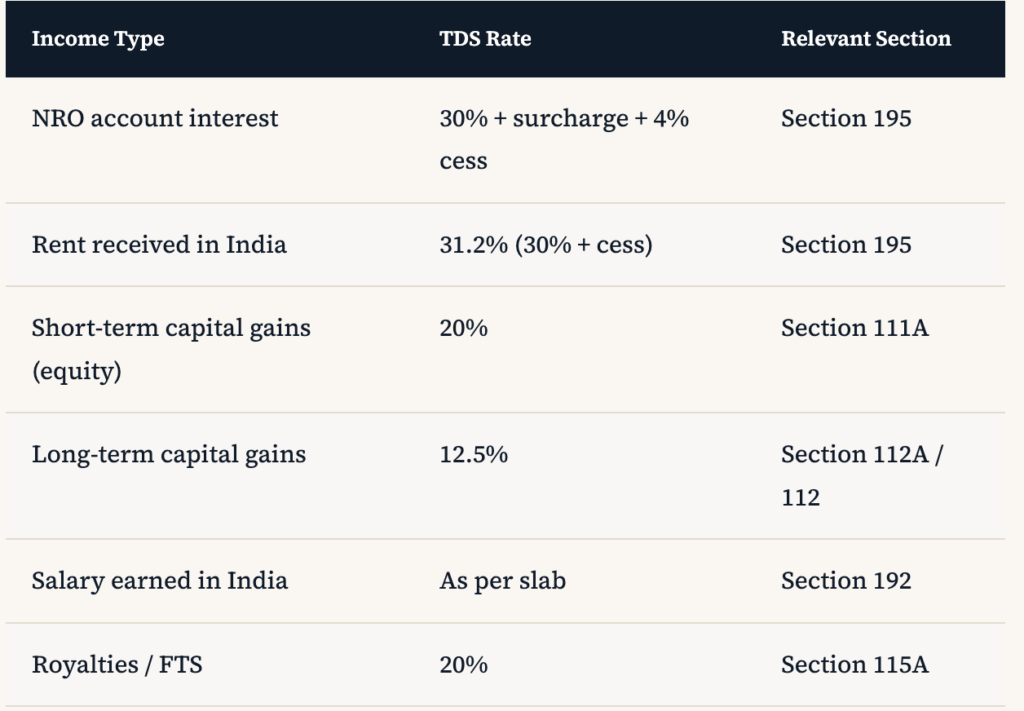

- Interest on NRO accounts: Interest earned on NRO (Non-Resident Ordinary) savings or fixed deposits is taxable. TDS is deducted at 30% (plus surcharge and cess) by the bank.

- Interest on NRE and FCNR accounts: Fully exempt from Indian income tax — one of the most valuable exemptions for NRIs.

- Dividends from Indian companies: Taxable at applicable rates, with TDS deducted at source.

- Royalties and fees for technical services: Paid from India are taxable under Section 115A at 20%.

- Lottery, puzzle, or game winnings: Taxable at a flat 30%.

Income That Is Exempt for NRIs

- Interest on NRE savings and fixed deposit accounts

- Interest on FCNR (Foreign Currency Non-Resident) accounts

- Interest on government notified bonds and savings certificates

- Long-term capital gains from reinvestment in specified assets (Sections 54, 54EC, 54F)

- All income earned or received outside India (while maintaining NRI status)

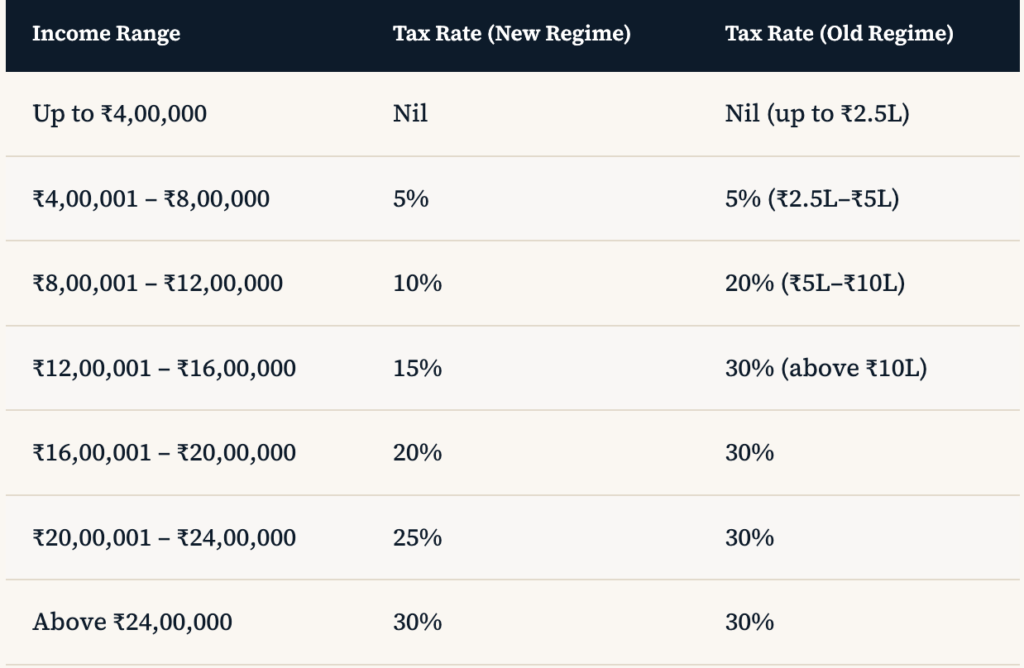

NRI Tax Slabs for FY 2025-26 (AY 2026-27)

NRIs use the same tax slab structure as resident Indians. The New Tax Regime is now the default under the Finance Act 2025, unless you explicitly opt for the Old Regime.

A Health & Education Cess of 4% applies on the total tax. Surcharge applies at 10% for income above ₹50 lakh, 15% above ₹1 crore, 25% above ₹2 crore, and 37% above ₹5 crore.

Special Flat Rates for Certain NRI Income

Certain income types are taxed at flat rates regardless of your total income or the slab system:

• Investment income (NRO interest, dividends from Indian companies) — 20% (Section 115E)

• Long-term capital gains on equity & MFs — 12.5% above ₹1.25 lakh (Section 112A)

• Short-term capital gains on equity — 20% (Section 111A)

• Long-term capital gains on property/debt MFs — 12.5% without indexation

• Royalties and FTS — 20% (Section 115A)

If you have a DTAA (Double Taxation Avoidance Agreement) with your country of residence, you can often get TDS deducted at a lower treaty rate instead. This requires submitting a Tax Residency Certificate (TRC) and Form 10F to the payer. Our team at FinCirc India handles this entire process.

Key Deductions Available to NRIs

NRIs can claim several deductions under Chapter VIA of the Income Tax Act, though the list is more restricted than for residents — especially under the New Regime.

- Section 80C (up to ₹1.5 lakh): Life insurance premium, ELSS (Equity Linked Saving Schemes), principal repayment on home loan for Indian property

- Section 80D: Health insurance premiums for self, spouse, and children

- Section 80E: Interest on education loan for higher studies

- Section 80G: Donations to approved charities in India

- Section 24(b): Interest on home loan (₹2 lakh limit for self-occupied property)

- Capital Gains Exemptions: Sections 54, 54EC, 54F — reinvesting gains into another house or specified bonds within prescribed timelines

Deductions NOT Available to NRIs

NRIs cannot claim deductions for PPF contributions, NSC, Senior Citizen Savings Scheme, or standard deduction from salary under the New Regime. Under the New Regime, most Chapter VIA deductions are also unavailable. Always consult a CA before choosing your tax regime — the wrong choice can cost significantly.

NRI Tax on Property Sale in India

Selling a property in India as an NRI triggers significant compliance obligations, often underestimated.

The buyer is required to deduct TDS at 12.5% on the sale value (for long-term capital gains) or 30% (for short-term gains), regardless of the actual gain. This is different from the rules for resident sellers. If you hold the property for more than 24 months, it qualifies as Long-Term Capital Asset, and gains are taxed at 12.5% without indexation.

To reduce or eliminate TDS, you can apply for a Lower Deduction Certificate under Section 197 from the Income Tax Department before the sale. FinCirc India routinely helps NRI clients obtain this certificate, significantly improving cash flow at the time of sale.

NRI Mutual Fund Taxation

NRIs can invest in Indian mutual funds (subject to fund-specific restrictions). The tax treatment mirrors that for resident Indians in terms of holding periods, but TDS applies differently:

- Equity mutual funds (Long-Term, held >1 year): 12.5% on gains above ₹1.25 lakh

- Equity mutual funds (Short-Term, held <1 year): 20%

- Debt mutual funds (Long-Term, held >3 years): 12.5% without indexation

- Debt mutual funds (Short-Term): As per slab rate