If you are an NRI earning income from India, there is a strong chance you are being taxed twice on the same money — once in India, and once in the country where you live. The Double Taxation Avoidance Agreement (DTAA) was specifically designed to prevent this. Here is a complete, advisor-level guide to understanding, claiming, and maximising DTAA benefits in India.

What Is DTAA and Why Does It Exist?

The Double Taxation Avoidance Agreement (DTAA) is a bilateral tax treaty signed between India and another country to ensure that individuals and companies are not taxed twice on the same income — once in the country where the income is earned, and again in the country where they reside.

India has signed comprehensive DTAAs with over 90 countries, including all major NRI-destination nations. These treaties are incorporated into Indian tax law under Section 90 of the Income Tax Act, which empowers taxpayers to apply whichever is more beneficial — the DTAA rates or the domestic rates.

The Core Principle of DTAA

If a provision of a DTAA is more beneficial to a taxpayer than the corresponding provision of the Income Tax Act, the taxpayer has the right to choose the DTAA provisions. This is established by Section 90(2) of the Income Tax Act, 1961. You are never forced to use the domestic rate when a treaty offers a lower one.

How DTAA Relief Works: Two Methods

Method 1 — Exemption Method

Under this method, income is taxed in only one of the two countries. The other country grants a full exemption. This is the most straightforward relief — if your income is taxed in India under the treaty, your country of residence exempts it from local tax, and vice versa.

Method 2 — Tax Credit Method (Foreign Tax Credit)

Under this method, the income is taxed in both countries, but the country where you reside grants a credit for the taxes already paid in India. So if India deducted ₹50,000 in TDS on your rental income and your country’s tax on that income would be equivalent to ₹80,000, you only pay the difference of ₹30,000 locally.

India uses both methods depending on the specific treaty and type of income. Most DTAAs with developed nations use the tax credit method for most income types.

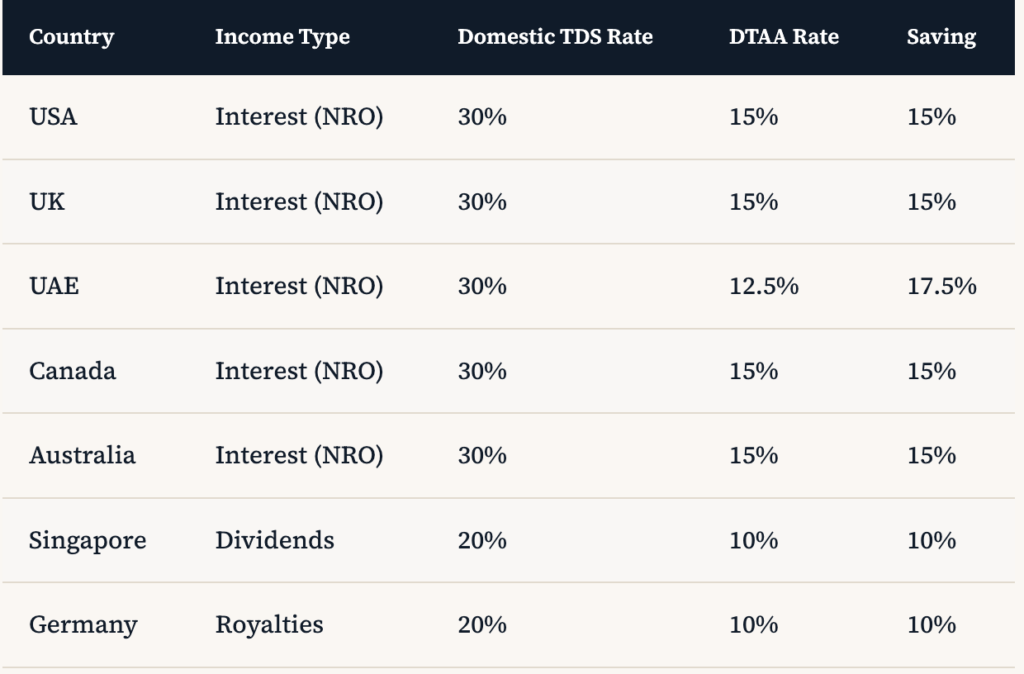

DTAA Rates vs Domestic TDS Rates — Key Comparisons

These savings are real money. For an NRI with ₹30 lakh in NRO deposits earning ₹2.4 lakh in interest, the DTAA rate (say, 15% for a US NRI) means paying ₹36,000 in TDS instead of ₹72,000 — saving ₹36,000 annually on just one income source.

How to Claim DTAA Benefits in India: Step-by-Step

Obtain a Tax Residency Certificate (TRC)

A TRC is the foundation of any DTAA claim. It is issued by the tax authority of your country of residence confirming that you are a tax resident there. For example, US NRIs obtain a Certificate of Residence from the IRS. UAE NRIs get one from the Federal Tax Authority. The TRC must be valid for the relevant financial year.

Fill and Submit Form 10F Online

Form 10F is a self-declaration form required by Indian tax law under Section 90(5). It contains your name, address, tax identification number (TIN) in your resident country, period of residence, and status. Since 2023, Form 10F must be filed online on the Income Tax e-filing portal (NRIs without PAN have a special procedure). FinCirc India files this on your behalf.

Submit TRC + Form 10F to the Payer

Before any payment is made (rent, interest, dividends), you must provide the TRC and Form 10F to the Indian payer (your bank, tenant, company). The payer is then authorised to deduct TDS at the lower DTAA rate instead of the domestic rate.

Report DTAA Benefits in Your ITR

When filing your Indian ITR, you must disclose all DTAA benefits claimed in the relevant schedules. This is where errors commonly occur — wrong treaty article numbers, incorrect income characterisation, or omitting the benefit claim entirely.

Claim Foreign Tax Credit in Your Resident Country

File your return in your country of residence and claim the Indian taxes paid as a foreign tax credit. The mechanism depends on the domestic law of that country and the treaty articles — your FinCirc India advisor coordinates this with advisors in your country of residence if needed.

DTAA with Key NRI Destination Countries

India–USA DTAA

One of the most utilised treaties. The India–US DTAA covers interest (taxed at max 15% in India), dividends (15%), and royalties (10–15%). US NRIs benefit particularly on NRO interest, which would otherwise attract 30% TDS. Social Security payments and pension income from India also have treaty provisions. NRIs must also comply with US FBAR and FATCA reporting for Indian accounts.

India–UAE DTAA

Since the UAE imposes zero personal income tax, this treaty is especially significant. The India–UAE DTAA limits Indian TDS on interest to 12.5% and dividends to 10%. UAE residents can claim these lower rates, effectively reducing their Indian tax burden substantially. The UAE issued Tax Residency Certificates through the Federal Tax Authority.

India–UK DTAA

The India–UK DTAA limits TDS on interest to 15% and dividends to 15%. UK residents can claim a credit for Indian taxes paid while filing their Self Assessment return with HMRC. Pensions and salary from India have specific sourcing rules under this treaty.

India–Canada DTAA

Similar to the US treaty in structure. Interest is capped at 15% TDS. Dividends at 15% (25% if the recipient controls at least 10% of the paying company). Canadian NRIs must also report Indian assets under their Foreign Income Verification Statement (Form T1135).

What If My Country Has No DTAA with India?

If India does not have a DTAA with your country of residence, Section 91 of the Income Tax Act provides unilateral relief. You can claim a deduction in India for taxes paid in the other country if that country taxes income from India at a rate not less than the Indian rate. The relief under Section 91 is typically less generous than a treaty, making it all the more important to structure your affairs correctly if you reside in a non-treaty country.

Common DTAA Mistakes That Cost NRIs Money

- Not submitting TRC and Form 10F to the bank in time — Results in TDS at 30% when 15% was the applicable rate. You then have to file an ITR and wait for a refund.

- Submitting an expired TRC — A TRC must be valid for the year in which the income arises. Many NRIs use TRCs from the previous year.

- Treating all income as benefiting from the same DTAA article — Different income types (interest, dividends, royalties, capital gains, business profits) are governed by different articles of the DTAA. Each has its own rate and conditions.

- Ignoring the Multilateral Instrument (MLI) — India has ratified the OECD’s Multilateral Instrument, which has modified several India DTAAs to introduce Principal Purpose Tests (PPT) and other anti-avoidance provisions. Some arrangements that previously worked under treaties may now be challenged.

- Failing to obtain a PAN — Without a PAN, TDS is deducted at 20% under Section 206AA, regardless of any DTAA benefit. Always maintain an active PAN as an NRI earning income from India.

DTAA Planning: When to Seek Professional Advisory

DTAA advisory goes beyond simply submitting a TRC and Form 10F. Professional DTAA planning at FinCirc India includes:

- Analysing the specific treaty articles applicable to your income mix

- Advising on the optimal account structure (NRE vs NRO) to minimise TDS exposure

- Coordinating India tax filings with your foreign return to maximise the Foreign Tax Credit

- Reviewing whether recent MLI changes affect your treaty position

- Advising returning NRIs on treaty-based planning before they trigger Resident status

- Representing clients in DTAA-related disputes with the Income Tax Department

Frequently Asked Questions — DTAA India

Accordion Content