Sending money from India to your foreign bank account sounds simple — but for NRIs, it is governed by the Foreign Exchange Management Act (FEMA), with specific limits, documentation requirements, and in some cases RBI approval. Getting it wrong can freeze your funds and attract penalties. This guide explains exactly how to do it right.

What Is FEMA and Why Does It Apply to NRIs?

The Foreign Exchange Management Act, 1999 (FEMA) regulates all cross-border transactions involving foreign exchange in India. It replaced the older FERA (Foreign Exchange Regulation Act) and governs NRIs in several critical ways:

- Which bank accounts NRIs can hold in India (NRE, NRO, FCNR)

- How much foreign currency can be held and repatriated

- How property transactions by NRIs must be structured

- Rules for foreign investments in India (FDI/FPI)

- Obligations when returning to India and converting accounts

FEMA vs Income Tax Act — Two Separate Frameworks

Many NRIs confuse FEMA and Income Tax Act compliance. They are entirely separate laws. You can be fully tax-compliant under the Income Tax Act and still be in violation of FEMA — and vice versa. Both must be addressed independently. FinCirc India handles both simultaneously so nothing falls through the cracks.

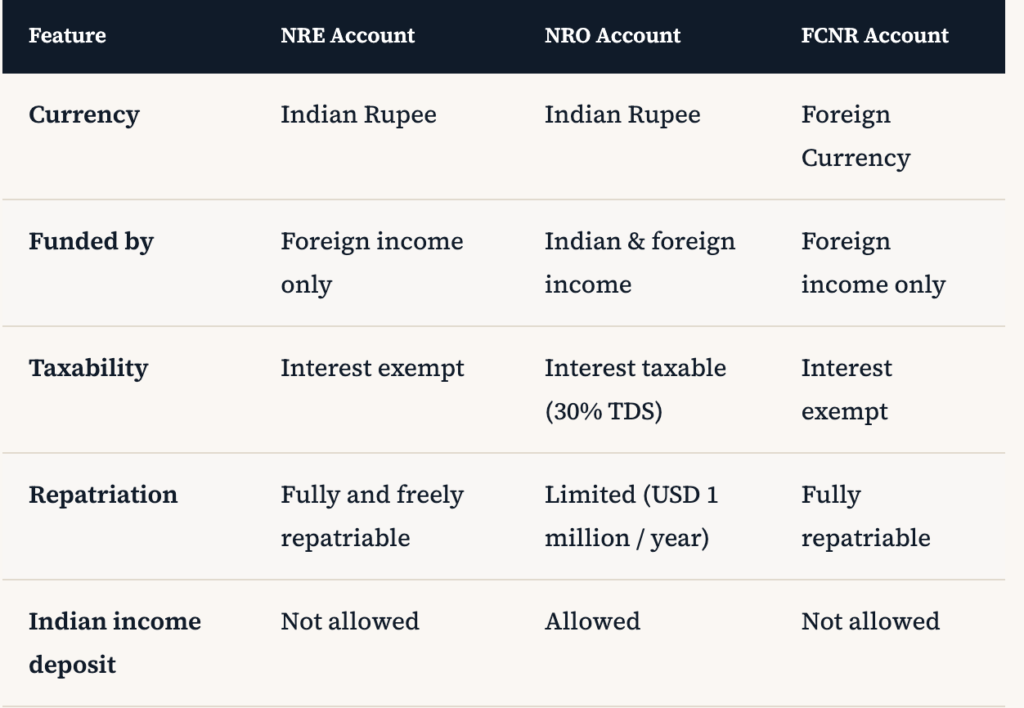

NRI Bank Accounts Under FEMA: NRE vs NRO vs FCNR

Fund Repatriation from NRO Accounts

The most common repatriation scenario for NRIs is transferring funds from their NRO account (which holds Indian income — rent, interest, dividends, property sale proceeds) to their foreign bank account.

Repatriation Limit from NRO Account

Under FEMA, the annual repatriation limit from an NRO account is USD 1 million per financial year (or equivalent). This applies to current income (rent, dividends, interest) as well as proceeds from sale of assets.

Documents Required for NRO Repatriation

- Form 15CA — Self-declaration form filed by the remitter (you or your CA) on the Income Tax portal before the remittance

- Form 15CB — Certificate issued by a Chartered Accountant certifying that the applicable taxes have been deducted and paid

- A2 Form — Remittance application to your bank

- PAN Card copy

- Tax payment challans, ITR copies, TDS certificates as applicable

- Source of funds documentation (sale deed, rental agreements, etc.)

The bank will not process a repatriation without Form 15CA/15CB for remittances above ₹5 lakh (with exceptions for certain categories). FinCirc India handles the entire 15CA/15CB certification process as part of our repatriation service.

Repatriation of Property Sale Proceeds

NRIs often sell inherited or purchased property in India and wish to repatriate the proceeds. This is subject to specific FEMA rules:

Rules for Repatriating Property Sale Proceeds

- The property must have been acquired in compliance with FEMA (i.e., it was not acquired when you were a resident using funds not allowed for NRIs)

- The property should ideally have been purchased using foreign exchange remittance or out of your NRE/NRO account

- Repatriation of sale proceeds is limited to the original investment amount in foreign exchange or to USD 1 million per year from NRO account, whichever is relevant

- For residential property: repatriation is generally allowed for up to 2 properties without RBI approval

- Agricultural land, plantation property, and farmhouse cannot be freely repatriated — RBI approval is required

Can I Repatriate More Than USD 1 Million?

Yes, but you need to apply to the Reserve Bank of India (RBI) through the Authorised Dealer Bank for remittances exceeding the USD 1 million annual limit. Such applications require detailed documentation including source of funds, tax compliance certificates, and the purpose of remittance. FinCirc India prepares and submits RBI applications on behalf of clients with large repatriation requirements.

FEMA Compliance for Returning NRIs

When you return to India and become a Resident under FEMA (which uses a different definition than the Income Tax Act), you are required to:

- Convert NRE and FCNR accounts to Resident accounts (or RFC — Resident Foreign Currency accounts) within a specified time

- Notify your bank of the change in residential status

- Close or redesignate NRO accounts — NRO accounts can continue as ordinary resident accounts

- Report overseas assets held in your Schedule FA of the ITR

- Comply with RBI’s reporting requirements for overseas investments and properties you continue to hold

Failure to convert accounts in time is a FEMA violation and can attract compounding penalties from the RBI’s Enforcement Directorate.

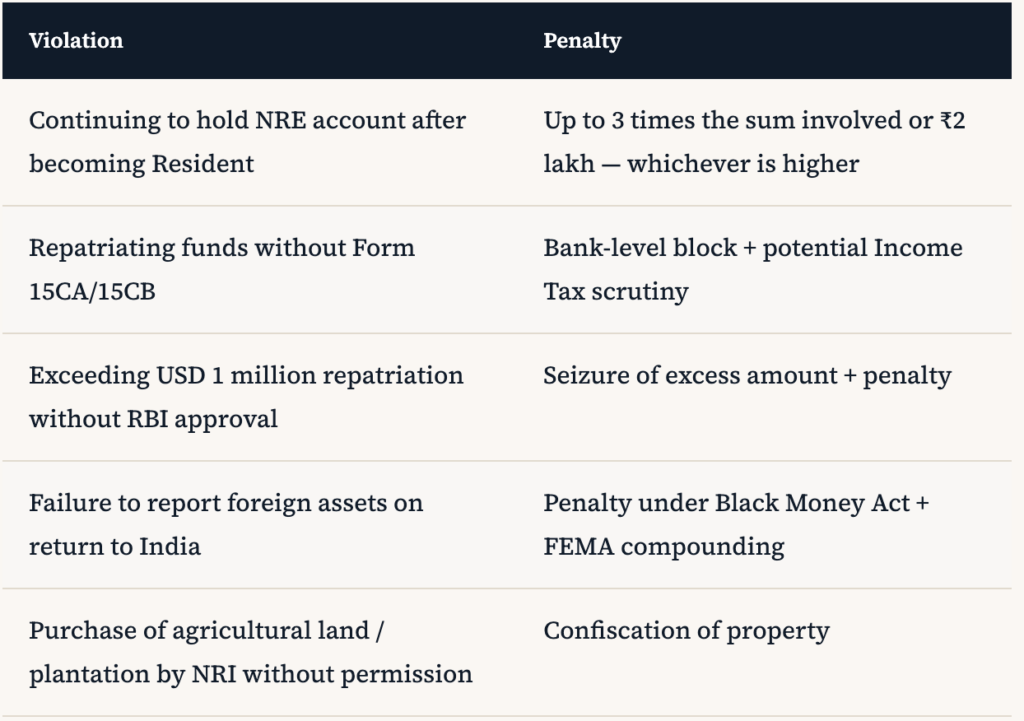

Common FEMA Violations and Penalties

Frequently Asked Questions — FEMA & Fund Repatriation

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.