Before any foreign remittance from India — whether you are repatriating rental income, property sale proceeds, or sending money abroad — your bank will ask for Form 15CA and in many cases Form 15CB. Without these documents, the remittance is simply not processed. This guide explains exactly what they are, when you need them, and how FinCirc India issues 15CB certificates and files 15CA for you — quickly and correctly.

What Is Form 15CA?

Form 15CA is a self-declaration form that must be submitted by the person making a foreign remittance from India. It is filed electronically on the Income Tax Department’s e-filing portal and serves as a declaration that applicable taxes on the remittance have been deducted and paid.

It was introduced under Rule 37BB of the Income Tax Rules, 1962 read with Section 195 of the Income Tax Act, to ensure that all cross-border payments are properly tracked and taxes accounted for before money leaves India.

What Is Form 15CB?

Form 15CB is a certificate issued by a Chartered Accountant (the CA must be a member of the Institute of Chartered Accountants of India — ICAI). The CA certifies:

- The nature and amount of the remittance

- Whether the remittance is taxable under the Income Tax Act or a DTAA

- The applicable TDS rate and the amount of tax deducted

- That taxes have been paid to the government before the remittance

The 15CB must be obtained before filing Form 15CA, as the 15CB certificate number and date are required in Form 15CA Part C.

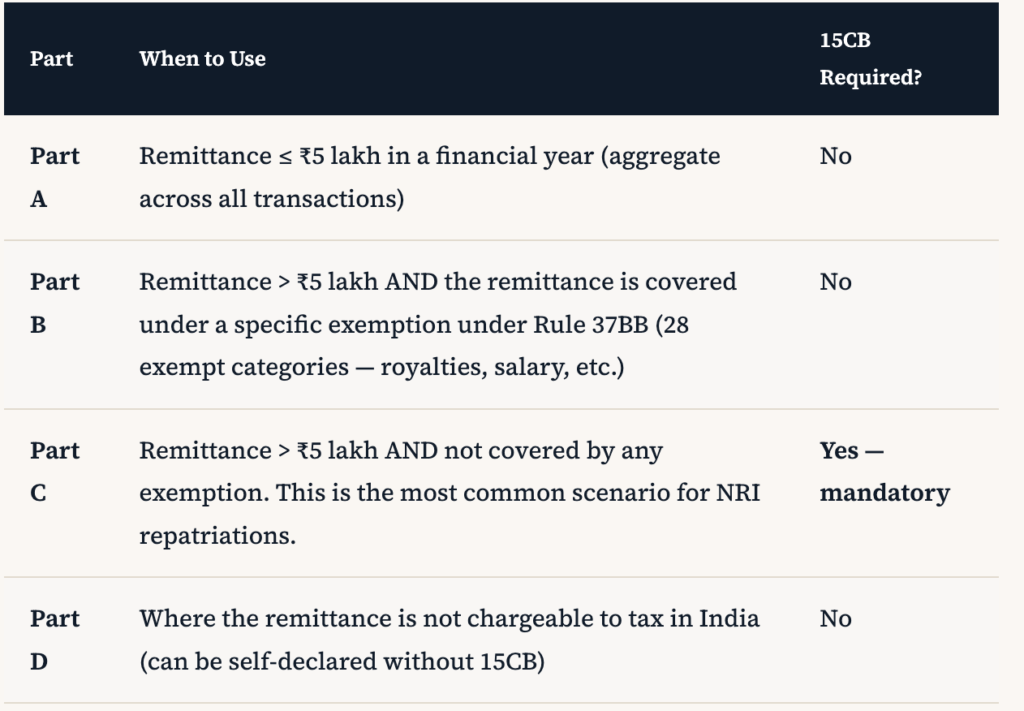

Four Parts of Form 15CA — Which Part Applies to You?

Most NRI Repatriations Require Part C

For rental income repatriation, property sale proceeds, NRO interest remittances, or any other remittance exceeding ₹5 lakh that does not fall under an exempt category, Part C of Form 15CA + a valid Form 15CB from a CA is mandatory. This is the scenario handled by FinCirc India for the vast majority of NRI clients.

The 28 Exempt Remittance Categories (No 15CB Required)

Rule 37BB lists 28 categories of payments that are exempt from the 15CA/15CB requirement entirely. Key exemptions relevant to NRIs include:

- Indian investment abroad in equity capital (less than 10% of paid-up capital)

- Remittance by a person who does not have a PAN (subject to conditions)

- Advance payment for international purchases of goods (subject to conditions)

- Travel expenses for business or pilgrimage

- Medical treatment abroad

- Donations to international institutions

- Salary payable to a non-resident for work done in India (if TDS deducted under Section 192)

For routine NRI repatriations of Indian income — rent, interest, sale proceeds — these exemptions do not apply. Form 15CA Part C and Form 15CB are required.

Step-by-Step: How Form 15CA/15CB Is Processed at FinCirc India

Document Collection from Client

You share the source of funds documentation — bank statements, TDS certificates, sale deed (for property), rental receipts, ITR, PAN — via our secure client portal.

Tax Computation & Treaty Analysis

Our CA computes the exact tax on the remittance, checks applicable DTAA provisions, confirms TDS deducted, and determines the correct Part of Form 15CA.

Form 15CB Issuance

Our ICAI-registered CA signs and issues Form 15CB, uploading it to the Income Tax portal and generating the Form 15CB Acknowledgement Number.

Form 15CA Filing (Part C)

Using the 15CB details, we file Form 15CA Part C on the Income Tax e-filing portal on your behalf. You receive the 15CA Acknowledgement Number.

Bank Submission & Remittance Execution

You submit the 15CA and 15CB documents to your bank’s NRI desk along with the A2 form. The bank processes the foreign remittance — typically within 2–3 working days.

Form 15CA/15CB for Property Sale: Special Considerations

NRIs selling property in India face a double compliance requirement — the buyer must deduct TDS on the sale consideration under Section 195, and the NRI must obtain Form 15CA/15CB to repatriate the net proceeds from the NRO account to their foreign account.

Lower TDS Certificate Before the Sale

Before completing a property sale, NRIs should apply for a Lower Deduction Certificate under Section 197. Without it, the buyer deducts TDS at 12.5–30% on the entire sale consideration (not just the gain). A Section 197 certificate limits TDS to the actual tax on gains — often significantly less. FinCirc India handles Section 197 applications as part of our property sale service, ensuring maximum cash in your hands at closing.

Online vs Offline: How Form 15CA/15CB Works Today

Since 2021, both Form 15CA and Form 15CB are filed electronically on the Income Tax e-filing portal. The CA must be registered on the portal as a Chartered Accountant (with valid ICAI membership number) to upload Form 15CB. Physical copies of both forms are then submitted to the bank.

The entire process can be done without the NRI being in India. FinCirc India has a streamlined remote process — you share documents digitally, we file everything electronically, and you receive the signed PDF forms to submit to your bank’s NRI remittance desk.

Frequently Asked Questions — Form 15CA/15CB

Accordion