TCS on Foreign Remittances has become a crucial concept for anyone engaged in cross-border transactions, especially under India’s Liberalized Remittance Scheme (LRS). The scheme allows individuals to send money abroad for purposes like education, medical treatment, travel, or investments. However, the government’s requirement to collect tax at source on such remittances aims to regulate and closely monitor the outflow of funds from India. Understanding these compliance rules from the very beginning can help avoid confusion, delays, and costly mistakes—just like the entrepreneur who faced unexpected hurdles when remitting his international earnings.

What is TCS?

TCS (Tax Collected at Source) is a provision under the Income Tax Act of India that requires the seller or remitter (foreign remittances) at the time of a transaction to collect a certain percentage of tax at the time of the sale or transaction. This tax is collected from the buyer or remitter at the time of making the payment, and the collected amount is then remitted to the government.

LRS Scheme Overview

The Liberalized Remittance Scheme (LRS) is a foreign exchange policy introduced by the Reserve Bank of India in 2004 to simplify and streamline the process of sending money abroad. This scheme was designed to ease the restrictions on international fund transfers imposed by the Foreign Exchange Management Act (FEMA), 1999. Under LRS, resident individuals are allowed to remit funds up to a specified limit for various permissible transactions related to both current and capital accounts.

How TCS Applies

In the context of foreign remittance transactions, a tax can be levied when you send money abroad. It’s important to understand that sending money doesn’t just mean transferring funds to another person—it could also include activities like traveling abroad, shopping internationally, investing overseas, purchasing assets, and more.

The Liberalized Remittance Scheme (LRS) facilitates international transactions with ease.

Recent Update on Tax for Foreign Remittance

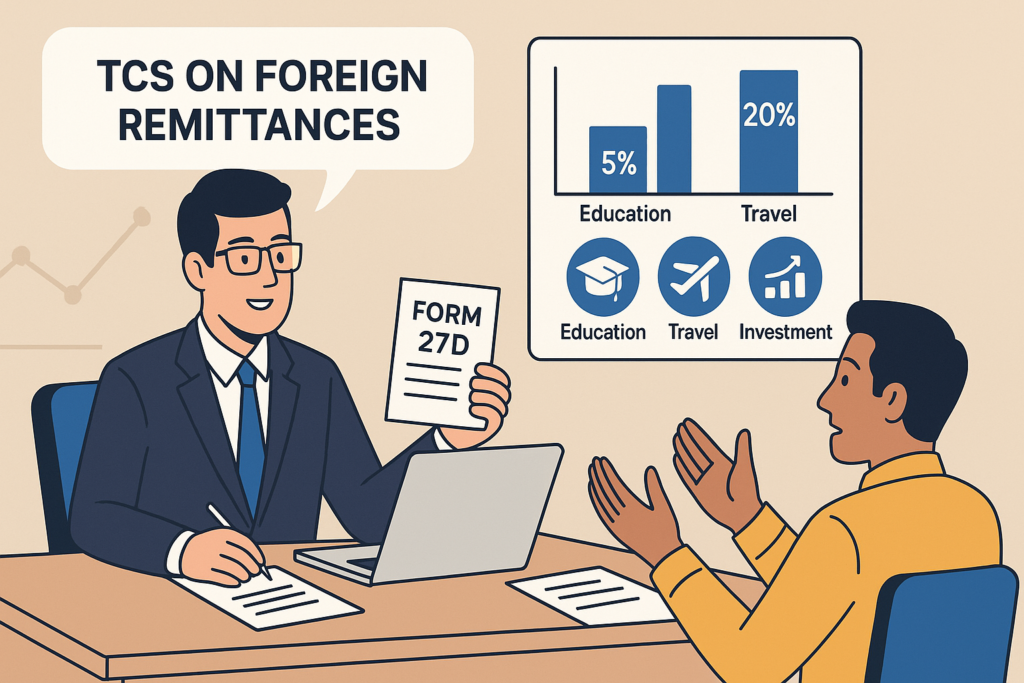

Prior to Budget 2023, foreign equity investments under the LRS attracted a 5% TCS for remittances exceeding ₹7 lakh. However, in the Budget 2023, Finance Minister Nirmala Sitharaman announced changes to the TCS structure. Starting from October 1, 2023, the TCS rate for foreign remittances related to foreign equity investments and overseas tour programs will increase to 20% for amounts exceeding ₹7 lakh, up from the previous rate of 5%.

Type of Remittance | Rate before 1st October 2023 | New Rate (Effective from 1st October 2023) |

Case 1: For education (education loan from a financial institution) | 0.5% on the amount or aggregate amount exceeding ₹7 Lakh | Nil up to ₹7 Lakh, 0.5% on amount above ₹7 Lakh |

Case 2: For education (other than Case 1 above) | 5% on the amount or aggregate amount exceeding ₹7 Lakh | Nil up to ₹7 Lakh, 5% on amount above ₹7 Lakh |

Case 3: Overseas tour package | 5% with no threshold limit | 5% up to ₹7 Lakh, 20% on amount exceeding ₹7 Lakh |

Case 4: Any other remittance | 5% on the amount or aggregate amount exceeding ₹7 Lakh | Nil up to ₹7 Lakh, 20% on amount above ₹7 Lakh |

TCS Applicability for NRIs

TCS is levied primarily on Indian residents under LRS. Non-Resident Indians (NRIs) enjoy extensive exemptions: No TCS on repatriation of up to USD 1 million per annum from NRO to NRE accounts, including after-tax Indian income like rentals or pensions. This is as per FEMA 1999, only RBI Form 15CA/CB for more.

However, NRIs remitting as residents (say, prior to status change) or making LRS using Indian accounts are subject to regular rates. Overseas debit/forex card expenditure invites TCS, whereas overseas credit card utilization is deferred. Per RBI’s Master Direction on Remittances (updated September 2025), NRIs should report residential status correctly so that they can avail of these privileges, avoiding inadvertent deductions.

How TCS is Paid

Collection of TCS:

- Banks/Remittance Service Providers: When you initiate a remittance under the Liberalized Remittance Scheme (LRS), the bank or remittance service provider processes the payment. For transactions subject to TCS, they will automatically collect the tax at the prescribed rate.

For example, if you are remitting more than ₹7 lakh for a foreign investment, the bank will collect the TCS at the applicable rate (5%, 20%, or 0.5% depending on the purpose).

Mode of Payment:

- The TCS is typically deducted from the amount being remitted. This means if you are sending ₹10 lakh and the TCS rate is 5% on amounts exceeding ₹7 lakh, the bank will deduct ₹15,000 (which is 5% of ₹3 lakh) from your ₹10 lakh and transfer the remaining amount abroad.

- TCS Amount: The collected tax is paid to the government, but you, as the remitter, are given credit for it. You do not need to pay this separately; it is collected and remitted by the bank.

TCS Certificate:

- After collecting TCS, the bank or remittance service provider will issue a TCS certificate (usually Form 27D). This certificate will show the amount of tax collected and remitted to the government on your behalf.

- This certificate will help you when filing your Income Tax Return (ITR), as the TCS amount will be considered as advance tax and can be adjusted against your total tax liability.

Key Compliance Steps

1.Understand the TCS Applicability: Before initiating any remittance, check if your transaction falls under TCS provisions, particularly if the amount exceeds ₹7 lakh or is for specific purposes like foreign equity investments or overseas tour packages.

2. Ensure Accurate Remittance Documentation: Keep track of all the documents related to your remittance transaction, including the TCS certificate (Form 27D) issued by the bank. This will be vital for claiming the TCS amount as advance tax.

3.Check the Updated TCS Rates: From October 1, 2023, be mindful of the new TCS rates for foreign remittances. Ensure that the remittance service provider deducts the correct amount according to the revised rates.

4.File Income Tax Return: When filing your ITR, ensure to include the TCS amount under the “advance tax paid” section to get credit for the tax already deducted and remitted to the government.

5.Monitor Foreign Remittance Limits: Stay within the prescribed limits of the LRS scheme for smooth processing of remittances. If you exceed the limits or exceed ₹7 lakh for a specific transaction, the revised TCS rates will apply.

Conclusion

The introduction of TCS on foreign remittances under the Liberalized Remittance Scheme (LRS) is a step towards improving tax compliance and monitoring international transactions. While it may seem like an additional burden, understanding the TCS rules and keeping track of the latest updates will ensure that the remittance process goes smoothly. By adhering to these compliance steps, individuals can avoid unnecessary delays and complications while sending money abroad, whether for personal or business purposes.

By following the guidelines and staying informed about any changes in tax rules, you can navigate the international financial landscape with confidence and ensure that your cross-border transactions comply with the law.

Bottom of Form