An entrepreneur who successfully sold his product to an international client. The payment came in large sums, and he was excited about the growth of his business. However, when he tried to remit the proceeds abroad, he faced an unexpected hurdle – tax! Confused, he asked his accountant for help, only to find out that he had to comply with TCS regulations under the Liberalized Remittance Scheme (LRS). The next few weeks were spent navigating through complex tax rules, and this led to several costly delays.

This is where understanding TCS compliance becomes essential for anyone involved in cross-border transactions. In India, the Liberalized Remittance Scheme (LRS) allows individuals to remit money abroad for specific purposes, like education, medical treatment, or investments. However, the government has imposed a Tax Collected at Source (TCS) on these foreign remittances, aimed at regulating and monitoring the flow of funds out of India

Let’s known the compliance details from the start?

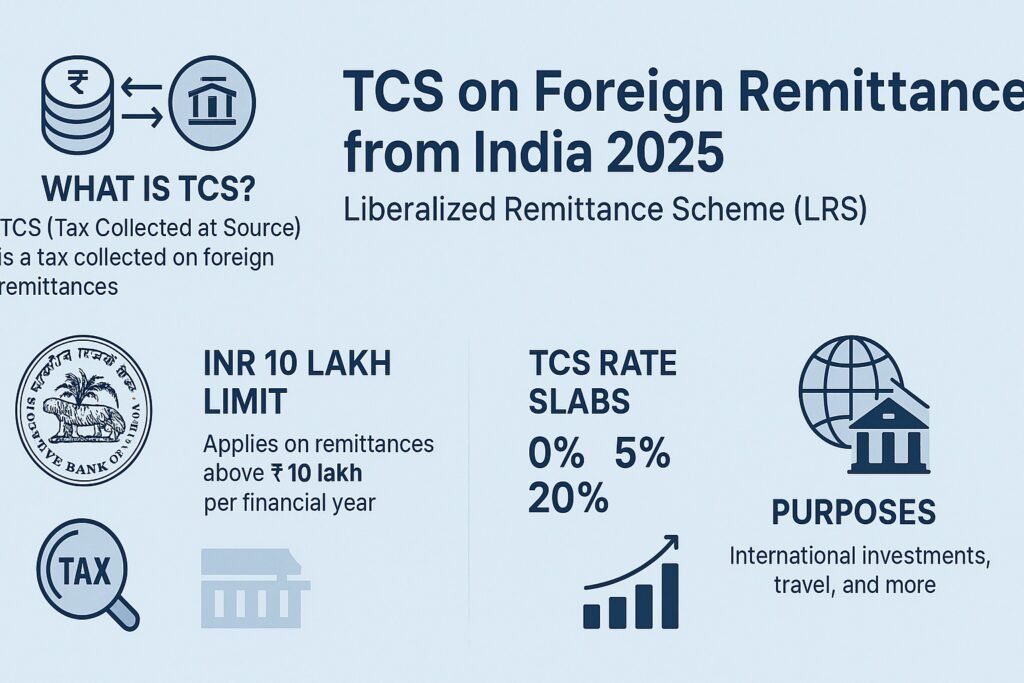

What is TCS on Foreign Remittance?

TCS (Tax Collected at Source) is a provision under the Income Tax Act of India that requires the seller or remitter (foreign remittances) at the time of a transaction to collect a certain percentage of tax at the time of the sale or transaction. This tax is collected from the buyer or remitter at the time of making the payment, and the collected amount is then remitted to the government.

The Liberalized Remittance Scheme (LRS) is a foreign exchange policy introduced by the Reserve Bank of India in 2004 to simplify and streamline the process of sending money abroad. This scheme was designed to ease the restrictions on international fund transfers imposed by the Foreign Exchange Management Act (FEMA), 1999. Under LRS, resident individuals are allowed to remit funds up to a specified limit for various permissible transactions related to both current and capital accounts.

In the context of foreign remittance transactions, a tax can be levied when you send money abroad. It’s important to understand that sending money doesn’t just mean transferring funds to another person—it could also include activities like traveling abroad, shopping internationally, investing overseas, purchasing assets, and more.

Budget 2025 Updates: New Thresholds & Rates

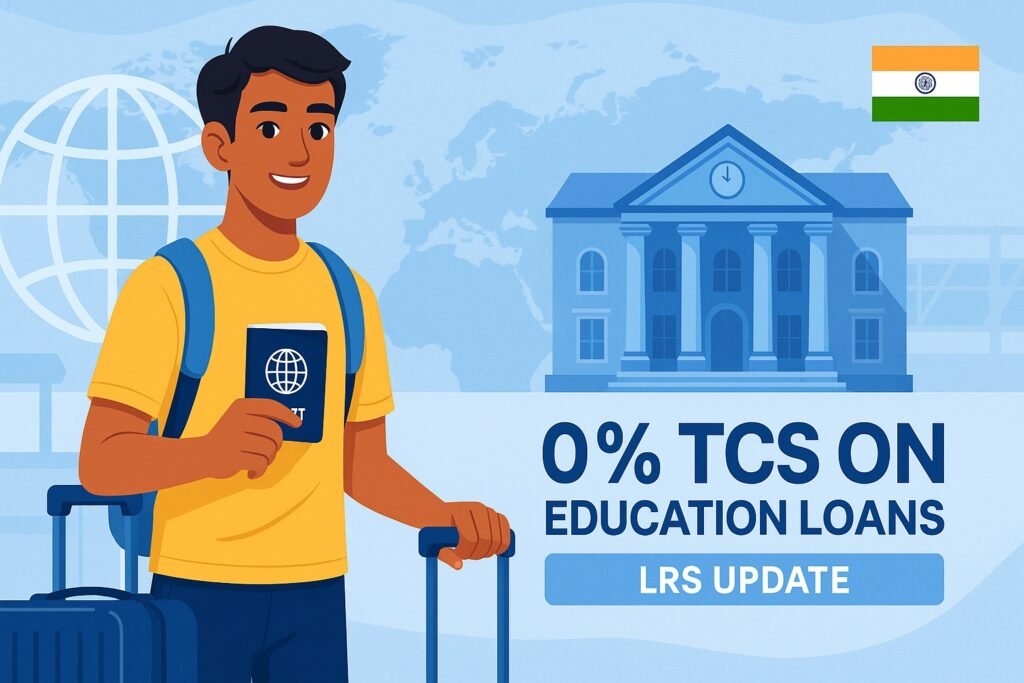

Budget 2025, presented in February 2025, brought some significant relief to outbound remittances, w.e.f. April 1, 2025. The limit for the applicability of TCS increased from INR 7 lakh to INR 10 lakh in the majority of categories, protecting regular transfers such as maintenance of family or minor medical treatments from instant tax. Besides, remittances for education through loans from notified banks and financial institutions (falling under Section 80E) now face 0% TCS, as against earlier rates, benefiting students pursuing international degrees.

Revised rates, as per CBDT Notification No. 28/2025 dated 15 March 2025, are:

Remittance Purpose | TCS Rate Structure (FY 2025-26) |

Education (via recognized loan) | 0% on entire amount |

Education/Medical (self/other-funded) | 0% up to INR 10 lakh; 5% above INR 10 lakh |

Overseas Tour Packages | 5% up to INR 10 lakh; 20% above INR 10 lakh |

Other Purposes (e.g., investments, gifts) | 0% up to INR 10 lakh; 20% above INR 10 lakh |

Exemptions from TCS

A number of circumstances exempt remittances from TCS, allowing crucial outflows without tax. Exemptions are:

- Education Loans: Nil TCS on amounts received by way of loans from scheduled banks or notified non-banking financial companies under Section 80E, directly supporting study abroad without remittance limits.

- Threshold Relief: No TCS on education or medical remittances up to INR 10 lakh per annum, aggregate of all such transactions.

- Overseas Credit Card Usage: Overseas expenses incurred by international credit cards abroad are still exempted until RBI provides RBI issues further guidelines, under a concession granted in July 2024 and extended to 2025. These include travel and incidentals expenses excluding LRS categorization.

- Non-LRS Transactions: Foreign investments in Indian mutual funds (through SEBI-registered schemes) for mutual fund or ETF investments are not subject to TCS since they fall outside direct LRS purview, according to FEMA guidelines.

How TCS is Collected & Paid

TCS collection is seamless and automated, handled by the remitting entity at the transaction’s outset. When making a transfer through a bank or authorized dealer, you’ll give purpose details (e.g., through Form A2) along with KYC documents such as PAN and passport. If your total FY remittances are more than INR 10 lakh, the provider deducts the appropriate TCS percentage from your account and remits quarterly to the government under CIN (Challan Identification Number).

Payment is not charged separately; it’s part of the transfer fee. For instance, on a INR 15 lakh investment remittance, INR 1 lakh (20% of INR 5 lakh surplus) is deducted, and your net outflow would be INR 16 lakh. Banks provide an immediate acknowledgement, and GST is payable only on service charges—none on the TCS itself. This process, as prescribed by Income Tax Rule 114B, makes real-time compliance possible, with your providers such as SBI or HDFC logging details in your transaction statement for easy tracking.

Checking, Claiming & Refund of TCS

Monitoring and reclaiming TCS is simple using digital tax tools. To confirm deductions:

- Form 27D: Get this certificate from the bank after the transaction, confirming the TCS amount and deposit details.

- Form 26AS/AIS: Access through the e-filing portal (incometax.gov.in) using your PAN—26AS breaks down credits, whereas AIS gives a wider transaction picture.

- TIS (Tax Information Statement): A new AIS extension for granular insights.

For claiming: While filing ITR (e.g., ITR-2/3 by 31 July), enter TCS under “Tax Payments” in Schedule TCS. It automatically offsets your liability; excess leads to a refund credited within 4-6 weeks through direct bank credit, according to CBDT timelines. Form 27D-26AS matching prevents discrepancies.

TCS Applicability for NRIs

TCS is levied primarily on Indian residents under LRS. Non-Resident Indians (NRIs) enjoy extensive exemptions: No TCS on repatriation of up to USD 1 million per annum from NRO to NRE accounts, including after-tax Indian income like rentals or pensions. This is as per FEMA 1999, only RBI Form 15CA/CB for more.

However, NRIs remitting as residents (say, prior to status change) or making LRS using Indian accounts are subject to regular rates. Overseas debit/forex card expenditure invites TCS, whereas overseas credit card utilization is deferred. Per RBI’s Master Direction on Remittances (updated September 2025), NRIs should report residential status correctly so that they can avail of these privileges, avoiding inadvertent deductions.

Smart Planning to Reduce TCS Impact

Minimize TCS without evasion by strategic timing and categorization:

- Stay Under Threshold: Limit aggregate remittances to INR 10 lakh/FY; split large ones over years if possible.

- Leverage Loans: Use education loans from eligible lenders for 0% TCS— 8-year repayment with 80E deductions.

- Purpose Optimization: spends properly (e.g., medical as opposed to general) for lesser 5% slabs; utilize credit cards overseas for back-loaded applicability.

- Refund Maximization: File ITR on time with all certificates; even if liability is minimal, net savings can be over 15-20% of TCS.

- Cost-Effective Providers: Mid-market rates are provided by platforms such as Wise or bank apps, reducing markups by up to 4x compared to conventional forex.

Frequenty Asked Question

Yes, at 5% above INR 10 lakh if self-funded; 0% if loan-financed from a recognized institution.

Same-day cancellations typically refund TCS instantly; otherwise, claim via ITR.

Yearly and overall for all LRS purposes for the person.

No, TCS is only for outward; inbound taxes are based on the sending country and FEMA regulations.

RBI-approved dealers (banks/partners) alone; unauthorized apps can’t handle LRS.