India’s rising debt levels, comprising both external and internal liabilities, have sparked concerns regarding the nation’s financial stability. Recent data highlights trends in the composition, growth, and implications of India’s debt, as well as the measures required to manage fiscal health effectively.

External Debt Overview

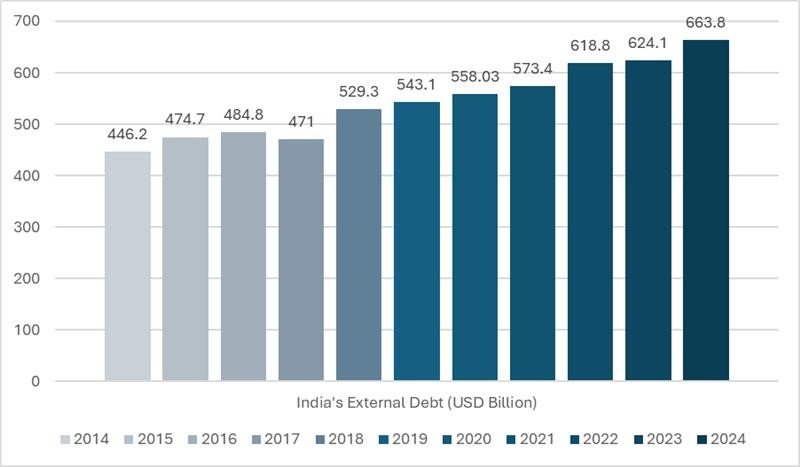

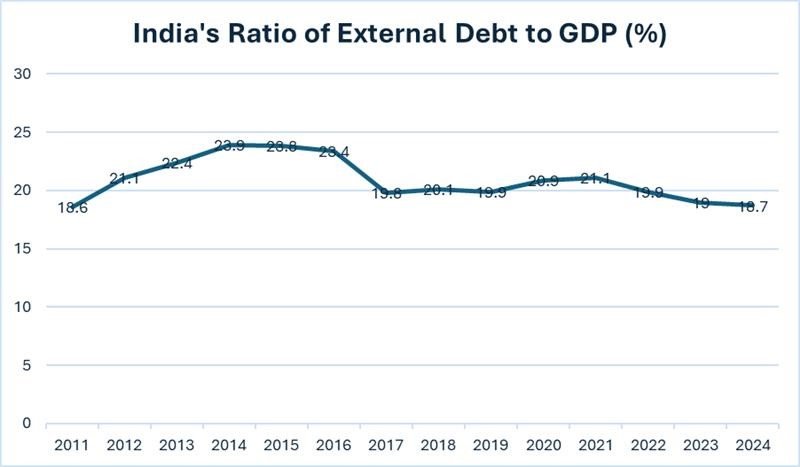

As of March 2024, India’s external debt reached $663.8 billion, marking an increase of $39.7 billion from the previous year. Adjusting for valuation effects from currency fluctuations, the real increase was even higher, at $48.4 billion. The debt-to-GDP ratio, however, showed improvement, dropping to 18.7% from 19% in March 2023. This is the lowest ratio recorded in 13 years and reflects the nation’s growing economic output relative to its external liabilities.

Composition and Currency Distribution

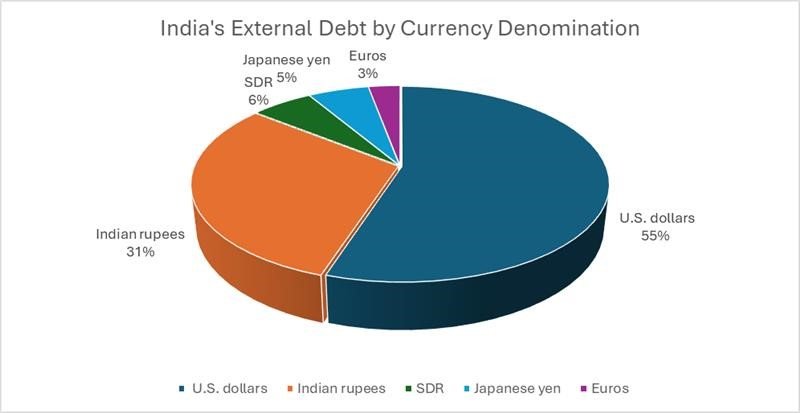

The largest portion of India’s external debt remains denominated in U.S. dollars (54.7%), followed by Indian rupees (30.5%), SDR (5.7%), Japanese yen (5.6%), and euros (2.9%) as of September 2023. The reliance on dollar-denominated liabilities underscores India’s vulnerability to exchange rate fluctuations, which can exacerbate debt repayment burdens.

Loans were the largest category within external debt, accounting for 32.9% of the total, followed by currency and deposits (23.0%), trade credit and advances (19.3%), and debt securities (16.5%). Among institutional borrowers, deposit-taking corporations, including banks, represented a significant share of 28.1% of total debt, with robust year-over-year growth of 14.3% in FY24.

Long-Term vs. Short-Term Debt

India’s long-term debt, defined as liabilities with an original maturity exceeding one year, increased by $45.6 billion year-over-year, reaching $541.2 billion as of March 2024. Short-term debt, on the other hand, declined, making up 18.5% of total external debt compared to 20.6% a year earlier. Improvements were also seen in the short-term debt-to-foreign exchange reserves ratio, which dropped to 19.0% from 22.2% in March 2023. This shift reflects India’s efforts to stabilize its debt profile and reduce reliance on short-term liabilities, which are more susceptible to global market volatility.

Debt Service and Sectoral Allocation

Debt service (principal plus interest) as a percentage of current receipts fell marginally, standing at 6.7% as of September 2023 compared to 6.8% in June 2023. Non-financial corporations accounted for 39.7% of total external debt, followed by deposit-taking corporations (27.1%), the general government (21.0%), and other financial corporations (7.3%).

Internal Debt Insights

India’s internal debt, which includes market loans, treasury bills, and other obligations, forms the larger component of the nation’s total liabilities. As of March 2024, internal debt and liabilities stood at ₹163.35 lakh crore, rising to ₹175.93 lakh crore by March 2025. Combined with external debt, the total public debt was projected to reach ₹185.27 lakh crore by the end of FY2024-25.

Composition of Internal Debt

Internal liabilities consist of loans raised in the open market, bonds issued to commercial banks and investors, and treasury bills. Additionally, it includes borrowings through non-negotiable securities issued to international financial institutions and non-interest-bearing securities held by state governments and banks. Public debt data is disclosed in the government’s Statement of Liabilities, detailing the assets created using these funds.

Historical Trends and Pandemic Impact

India’s total debt burden (internal and external) surged during the COVID-19 pandemic, reaching 88% of GDP in FY21, up from 74% in FY20. This sharp rise resulted from the government’s fiscal measures under the Atmanirbhar Bharat package, which were aimed at mitigating the economic fallout of the pandemic. These interventions caused a 14% increase in general government debt in FY21, the highest annual rise in two decades.

While debt-to-GDP ratios have since improved, reflecting an economic recovery, the pandemic highlighted structural vulnerabilities in India’s fiscal framework. The general government’s external debt rose to $148.7 billion by March 2024, representing a year-over-year increase of 11.5%. However, India’s general government debt-to-GDP ratio, at 82.5% in FY24, remains one of the lowest among major economies, second only to Germany.

Comparative Perspective and Future Outlook

India’s external debt-to-GDP ratio of 18.7% is significantly lower than that of advanced economies such as the United Kingdom (283.8%) and Japan (263.0%) , showcasing relative fiscal prudence. Projections by the Reserve Bank of India suggest that the general government debt-to-GDP ratio could decline further to 73.4% by FY31, driven by strategic realignment of spending and favorable interest rate conditions.

Despite positive indicators, challenges persist. The growing reliance on market borrowings and the substantial share of external debt in foreign currencies heighten India’s exposure to global financial shocks. To maintain fiscal resilience, the government must align debt growth with economic productivity and ensure that liabilities contribute to asset creation.

Conclusion

India’s rising debt reflects the complexities of balancing growth with fiscal discipline. While reductions in short-term liabilities and improvements in debt-to-GDP ratios are encouraging, managing the broader debt landscape requires sustained policy efforts. Effective debt management, coupled with measures to boost economic output, will be pivotal in safeguarding India’s financial stability and ensuring sustainable development in the coming years.