As a sailor, whether you are an Indian national cruising internationally or heading back to India after years away, knowing your tax requirements and bank solutions is essential. The very nature of your job usually entails staying away from India for longer stretches of time, which affects your residential status directly as well as your income tax and FEMA (Foreign Exchange Management Act) 1999 requirements. The following is an in-depth account as per the most recent provisions under Income Tax Act, 1961 (as updated as per Finance Act 2025), and FEMA norms as per August 2025. It includes residential status determination, tax on salary and other income, exemption and deductions, and non-resident account conversion (NRE and NRO) accounts. Remember that although the Draft Direct Tax Code (DTC) 2025 promises to rationalize rules, as yet this legislation is not enacted, and thus present legislation holds unless indicated otherwise.

We’ll address both resident and non-resident seafarers, highlighting key differences and practical scenarios. Always consult a tax professional for personalized advice, as individual circumstances vary

Determining Residential Status of Seafarers

Your residential status under the Income Tax Act determines the quantum of taxable income within India. For sailors, this is governed by Section 6 with special regard by way of time at sea.

Basic Rules for Residential Status

- Resident in India: You are a resident if:

- (a) You live in India for 182 days or more during the last previous year (PY), or

(b) You are present for 60 days or more during the PY as well as 365 days or more during the four prior years.

- (a) You live in India for 182 days or more during the last previous year (PY), or

- Nonetheless, for Indian nationals who are leaving India to work (including as crew members on vessels or as seafarers), the 60-day rule is suspended to 182 days. This exemption applies to you if you are leaving as a crew member or to work abroad.

- Non-Resident (NR): If neither condition above is met, you are a non-resident.

- Resident but Not Ordinarily Resident (RNOR): A resident is RNOR if they have been NR in 9 out of 10 previous years or stayed in India for 729 days or less in the 7 preceding years. RNOR status offers transitional benefits, taxing only India-sourced or business-controlled income.

Special Provisions for Seafarers

- The Central Board of Direct Taxes (CBDT) released clarifications through Circular No. 13/2017 and its later revisions that time on foreign vessels beyond Indian territorial waters is not included as a “stay in India.” It is included for Indian vessels if the vessel is within Indian waters.

- Rule 126 of Income Tax Rules: The duration of stay for crew members doesn’t include the arrival and leaving date from India. Count days using your Continuous Discharge Certificate (CDC) or passport.

- Amendment under Finance Act 2020: If your total income from Indian sources (excluding foreign income) is more than ₹15 lakh, 182 days is lowered to 120 days for deemed residency.

Scenario Example: The sailor who is on a foreign ship for 200 days during FY 2024-25 (AY 2025-26) with < ₹15 lakh Indian income is treated as NR, although he is on shore leave for 100 days within India.

Under FEMA, residential status is different—to be determined on intention to remain within India for an indefinite period (of over 182 days). The recent tribunal decision highlights that FEMA status changes upon arrival with a settlement intention, which could be prior to tax residency.

Taxation of Income for Resident and Non-Resident Seafarers

It is residential status and source of income-based taxation.

For Non-Resident Seafarers

- Only India-sourced income is taxable (e.g., rental income, interest from NRO accounts).

- Salary Taxation: Salary of non resident seafarers for services rendered outside India on a foreign ship is exempt if credited to an NRE or NRO account. This is per CBDT Circular 13/2017 and remains unchanged in 2025.

- If aboard an Indian vessel, salary could be taxable as India-sourced.

- Other income (e.g., capital gains from Indian assets) is taxable.

For Resident Seafarers

- Global income is taxable, including overseas salary.

- Residents and Ordinarily Residents (ROR): All income taxable

- RNOR: Foreign income non-exempt unless received from a business with control in India.

- Seafarers becoming residents (e.g., after retirement) must report worldwide income.

Updated till 2025: Salary tax regulations remain the same. Filing of ITR by NR seafarers with exempt salary is not necessary but recommended for refund or regularity purposes. New ITR-U accepts up to 48 months from end of AY to be filed.

Scenario Example: A non-resident seafarer earning $100,000 on a foreign ship (credited to NRE) pays no tax in India. If resident, the full amount is taxable under the new or old regime.

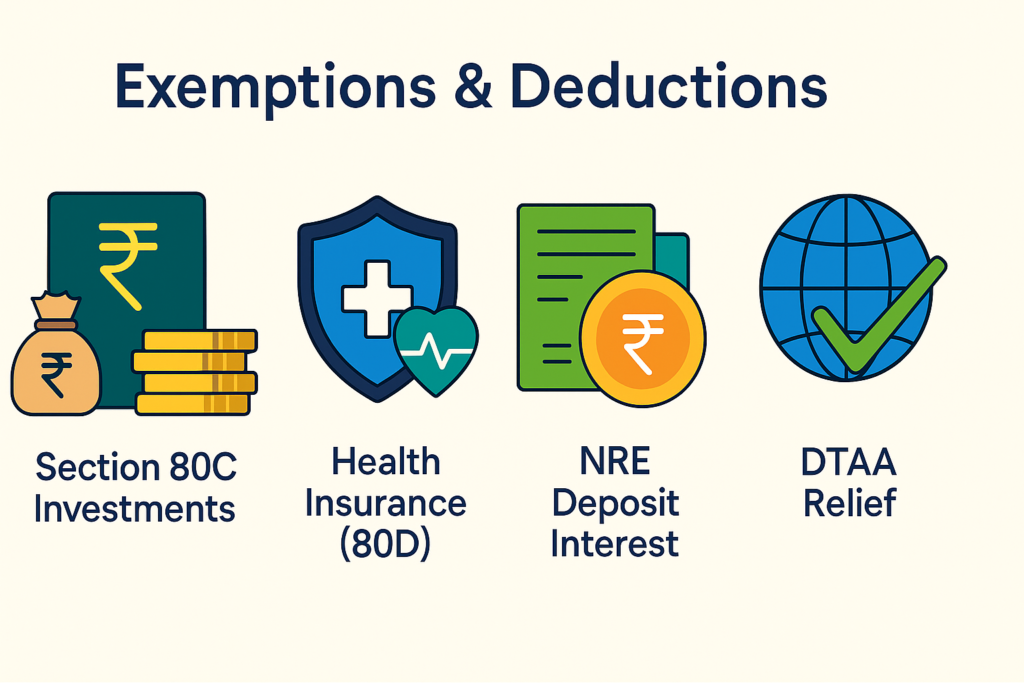

Available Exemptions and Deductions to Seafarers

Exemptions

- Section 10(15): Interest on NRE/FCNR deposits is tax-free for NR/RNOR seafarers.

- Salary Exemption for NR: As above, foreign ship salary exempt.

- Foreign income for RNOR/NR: Non-taxable.

- DTAA Benefits: If taxed abroad, claim relief under Double Taxation Avoidance Agreements.

Deductions

- Standard Deduction: ₹50,000 for salaried residents (including seafarers).

- Section 80C: ₹1.5 lakh maximum for investment such as PPF, ELSS (applicable to all statuses).

- Section 80D: Health premiums.

- HRA Exemption: If you are getting HRA and paying rent in India.

- For NR: Deductions limited to taxable Indian income.

- 2025 Changes: DTC 2025 suggests taxing short-term capital gains at 20% (instead of 15%) and bringing them into normal income, but exceptions such as NRE interest are unaffected.

Management of NRE and NRO accounts: Conversion under FEMA

FEMA governs banking and foreign exchange for NRIs, which include sailors.

Major Accounts

- NRE Account: For foreign earnings; fully repatriable, tax-free interest. Ideal for NR seafarers.

- NRO Account: For Indian income; interest taxable, repatriation up to USD 1 million/year after taxes.

Conversion Rules

- Becoming NR (e.g., employment on a ship overseas): Convert resident savings/accounts to NRO. Resident accounts are not permitted to be held by NR. Start NRE for foreign transfers.

- Becoming Resident (e.g., return seafarer): Re-classify NRE to Resident Foreign Currency (RFC) account (repatriable) or resident account. Convert NRO to resident. This needs to be done immediately upon shift in FEMA status.

- 2025 Updates: Urgent conversion emphasized by RBI; Delay possible with FEMA violations. Recent tribunal ruling elucidates that FEMA residency starts on return intention and affects gift and property dispositions. Limitations of repatriation remain unchanged.

Scenario Example: NR-seafarer liquidates SBI savings to NRO to convert rent income and sets up salary account in NRE. Upon return, NRE to RFC to maintain foreign currency benefit.

Conclusion

Low tax incidence applies to non-resident seafarers on foreign income with NRE accounts providing flexibility. Residents are subject to international tax with deductions allowed for use. Keep yourself updated by counting days through CDC, furnishing ITR where necessary, and converting accounts timely under FEMA. As changes in DTC 2025 are imminent, keep track through CBDT and RBI notices. On complex issues such as two-year residency or high income earned in India, consult professionals to steer clear of penalties. Bon voyage!

Frequently Asked Questions

It is not mandatory if you are not receiving taxable income. But filing is highly recommended as this facilitates processing of loans, issuance of visas, claiming of refunds as well as avoiding future disputes.

Regular due date: 31st July of the assessment year.

Belated ITR: Can be filed within 48 months using the new ITR-U option, though with a penalty.

- Passport and CDC (with details of sign-on/sign-off

- Contract of employment with shipping company.

- NRE/NRO bank account statements.

- Salary cheques or email from employers.

- Property and investment records.

It is exempt under Section 10(4)(ii) if you are a non-resident. Nevertheless, you report it under “Exempt Income” in the ITR.

It builds your financial track record in India. Guarantees that FEMA and Income Tax norms are followed. Serves as proof of NRI status if tax authorities question it.